November 2024 was a dynamic month in financial markets, shaped by two critical events: the U.S. presidential election and the Federal Reserve’s monetary policy meeting. These events influenced market movements, economic sentiment, and investment strategies. In this edition of Ceva Insights, we unpack how the recent election results and the Federal Reserve’s latest policy decisions are shaping market dynamics and influencing investor sentiment.

Key Highlights: Navigating November of 2024

Economic Overview: The Federal Reserve’s November 7 rate cut of 0.25% to 4.5%, combined with rising inflation at 2.6% and an uptick in unemployment to 3.9%, highlights a delicate balance between growth and inflation concerns.

Equities: U.S. equities surged in November, with small caps gaining nearly 11% and large caps rising 5.9%, driven by optimism around a Trump administration’s pro-business policies.

Fixed Income: The 10-year Treasury yield decreased to 4.175%, easing bond market pressures as markets responded positively to Scott Bessent’s appointment as Treasury Secretary.

Real Estate: Mortgage rates climbed to 6.81%, challenging affordability and dampening transaction activity, while inventory constraints and cautious buyer behavior added pressure to the housing market.

Economic Overview

November brought a mix of developments that highlight the delicate balance between growth and inflation.

Election Results: Donald Trump’s victory was widely seen as favorable for markets due to expectations of pro-business policies:

Deregulation across industries

Stable or lower taxes

Favorable conditions for U.S.-based businesses

Federal Reserve Actions: On November 7, the Fed cut interest rates by 0.25%, bringing the Fed Funds Rate to 4.5%. While this move was anticipated, it signaled a continued commitment to managing inflation and unemployment under their dual mandate.

Inflation and Unemployment: Core CPI rose slightly to 2.6% in October from 2.4% in September, tempering expectations of aggressive rate cuts in December or early 2025. Unemployment stood at 3.9%, up from 3.6% a year ago but indicative of a moderating labor market.

With the election and upcoming Fed policy decisions, November set the stage for increased volatility, especially as markets recalibrate expectations for fiscal and monetary policy.

Equities

U.S. equities rallied significantly in November after a challenging October, reflecting investor optimism.

Broad Market Gains: S&P 500: Rose 5.9%, driven by robust performances in financials and small caps.

Financials: The S&P 500 Financials Index gained 10.3%, reflecting optimism for improved conditions in lending and dealmaking.

Small Caps: The Russell 2000 soared nearly 11%, buoyed by expectations of pro-business policies from the incoming administration.

Global Disparity: Non-U.S. markets struggled under the weight of a stronger dollar, tariff concerns, and geopolitical uncertainties, with foreign equities lagging behind their U.S. counterparts.

These trends underscore the resilience of U.S. equities and the challenges facing international markets amid shifting trade and fiscal policies.

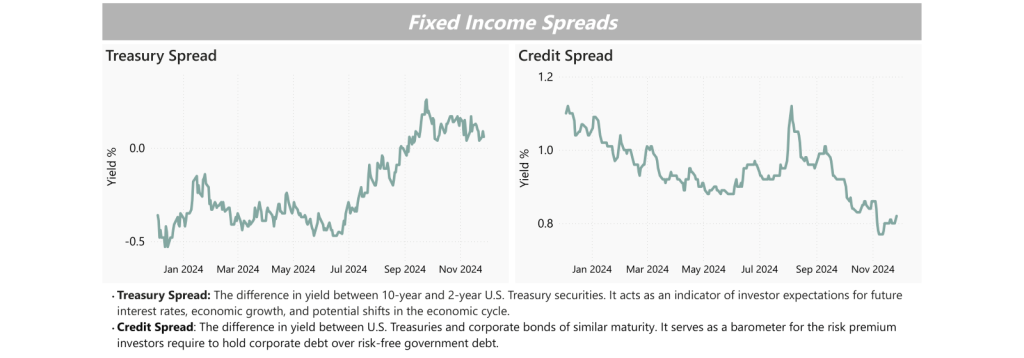

Fixed Income

The fixed income market experienced significant shifts in November as investors reacted to economic and political developments.

10-Year Treasury Yields: Fell from a mid-month high of 4.47% to 4.175% by month-end. Early fears of inflation tied to Trump’s policies were mitigated by the announcement of Scott Bessent as Treasury Secretary, whose moderate approach reassured markets.

Treasury Spread Dynamics: Yields declined sharply following Bessent’s appointment, reflecting optimism for stable fiscal management.

Credit Spreads: Tightened as market sentiment improved, with investors pricing in a tempered approach to fiscal expansion under the new administration.

The interplay of fiscal policies and leadership appointments will remain a focal point for bond investors in the coming months.

Real Estate

The residential real estate market in November 2024 continues to grapple with rising mortgage rates and evolving buyer behavior. While many anticipated that the Federal Reserve’s rate cut in September would lead to a drop in mortgage rates, the reality has been more nuanced. The average 30-year fixed mortgage rate climbed to 6.81% by month-end, reflecting the disconnect between the Fed’s actions and long-term lending rates.

The housing market remains constrained by limited inventory and ongoing affordability challenges. Unpredictable buyer behavior has added complexity, with some delaying purchases in hopes of rate relief while others proceed cautiously due to economic uncertainty. These dynamics underscore the continued pressure on the housing market as it navigates higher borrowing costs and shifting economic conditions.

Closing Remarks

November 2024 was defined by pivotal events that shaped market sentiment and set the tone for the months ahead. While U.S. equities surged on optimism around pro-business policies, fixed income markets found reassurance in stabilizing leadership appointments. However, the persistence of inflation and rising borrowing costs pose challenges for both equities and real estate.

As we look toward December, the interplay between fiscal policy, Fed decisions, and market expectations will likely lead to continued volatility. Maintaining a diversified investment strategy remains key to navigating these dynamic conditions.

Allen, Henry and Jim Reid. “November 2024 Performance Review.” Deutsche Bank Research, December 2, 2024

“Markets Daily: November 1 – November 30, 2024 Series.” Bloomberg, November 1 – November 30, 2024.

IMPORTANT DISCLOSURE: The information contained in this report is informational and intended solely to provide educational content to our clients and other readers that we find relevant and interesting. Opinions expressed are just that, and are current only as of the data of publication Nothing in this document should be construed as investment advice; we provide advice on an individualized basis only after understanding your circumstances and needs. The information presented in this newsletter is based on reports from Deutsche Bank and Bloomberg’s ‘5 Things You Need to Know to Start Your Day’ series. Data provided comes from sources we believe are reliable, but accuracy is not guaranteed. Discussion of sectors and the performance of region-specific equities and bonds generally refers to market indices. We use the S&P 500 to represent US large-cap; the Willshire Small Cap to represent US small-cap; the MSCI ACWI ex US to represent international equities; the US 10-year Treasury Yield to represent US Treasuries; the ICE BofA European Government Bond Index to represent European bonds; the ICE BofA US Corporate Index Effective Yield to represent investment-grade bonds; the ICE BofA US High Yield Index Effective Yield to represent high-yield bonds. Indices are unmanaged, are not subject to investment management fees or transaction costs, and it is not possible to invest in an index. Index performance can provide general information about how a particular region or investment has performed, but does not provide information about the performance of Ceva’s client portfolios. Actual client performance may differ materially from the index performance discussed. Past performance is not a guarantee of future results. Financial planning is a tool that can help clients consider different current and future scenarios and construct portfolios designed to meet specific goals and address specific risks. Financial planning does not guarantee a positive outcome or prevent loss. It’s important to revisit financial plans and the underlying assumptions of those plans regularly, and to make adjustments as needed to respond to changing circumstances.