May was a strong month for the markets. Stocks moved higher after the U.S. and China agreed to pause new tariffs for 90 days, which helped calm global trade tensions. At the same time, the Federal Reserve kept interest rates unchanged, giving investors more confidence that borrowing costs won’t rise further for now. As a result, both stock and bond markets performed well. Inflation showed signs of cooling, and fears of a recession eased a bit. Overall, it was a positive month for portfolios.

Even with the recent rebound, there are still reasons to stay cautious. Inflation remains above the Fed’s target, mortgage rates are still hovering near 7%, and home affordability continues to weigh on the housing market. In fixed income, long-term bond yields climbed—most notably the 30-year Treasury, which neared 5% for the first time in nearly two decades—as questions are raised about long-term debt sustainability. As we head into summer—a season that often brings lower trading volume and more volatility—it’s a good time to stay focused on long-term goals and avoid overreacting to short-term market shifts.

Key Highlights: Navigating May of 2025

- Economic Overview: The U.S. economy shrank slightly in Q1, but a temporary truce in the U.S.–China trade conflict and signs of easing inflation helped improve the overall outlook.

- Equities: Stock markets rallied sharply in May, with global and U.S. indexes climbing on reduced recession fears and improved investor confidence.

- Fixed Income: Long-term bond yields rose and credit spreads narrowed as risk appetite returned, though uncertainty surrounding U.S. budget deficits and long-term risks added some late-month uncertainty.

- Real Estate: Housing remained soft due to high mortgage rates, with affordability near historic lows, but rising home inventory and builder activity showed early signs of adjustment.

Economic Overview

Economic data in early 2025 painted a mixed picture. U.S. GDP contracted at a –0.3% annualized rate in Q1, largely due to businesses front-loading imports ahead of anticipated tariffs². This sets the stage for a potential period of stagnation as the tariff shock filters through and demand softens. In fact, if the full slate of import duties announced in April were to take effect after the current truce, recession risks would

rise.

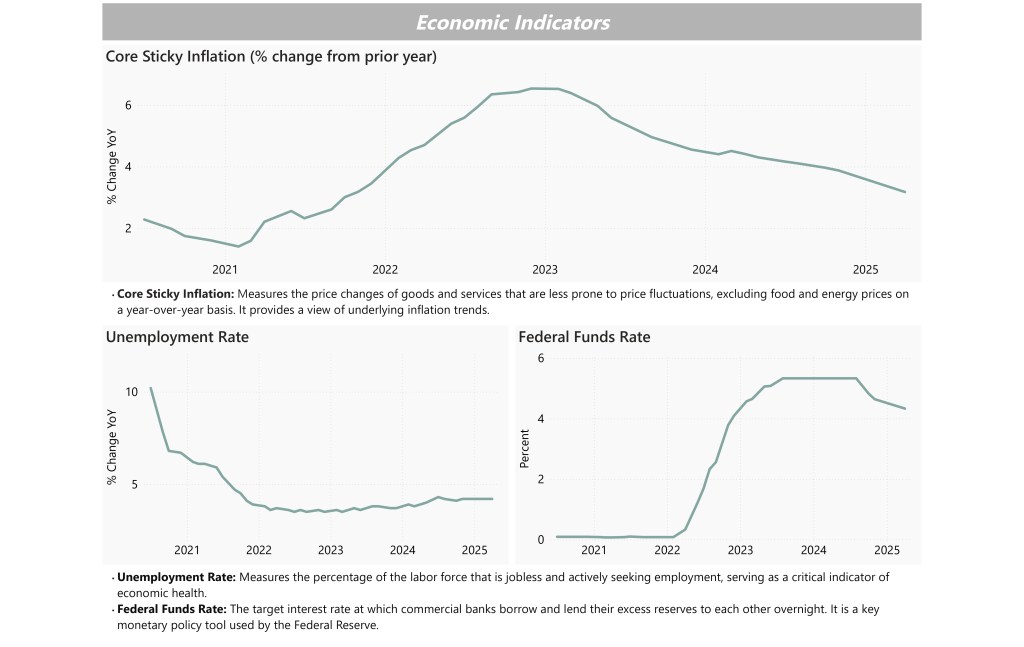

On a brighter note, trade tensions eased in May after Washington and Beijing agreed to roll back some tariffs and implement a 90-day pause in their trade war. This temporary truce removed a major overhang from the outlook, boosting business and investor sentiment. Inflation has shown tentative signs of improvement: the Fed’s core PCE index slowed to 2.6% year-over-year in March (from 3.0% in February)³. However, price pressures remain sticky, and Fed officials are wary that recent tariff-related cost increases could reverse the disinflation trend.

The Federal Reserve held interest rates steady in May, keeping the target rate at 4.25–4.50% (unchanged since the last hike in Dec 2024). Policymakers face a tricky balance between containing inflation and supporting growth. With unemployment still low around 4.2%, the Fed has signaled that future rate moves will depend on incoming data³. For now, the central bank appears content to wait and see, continuing its pause even as financial conditions tighten due to prior hikes and trade uncertainties.

Equities

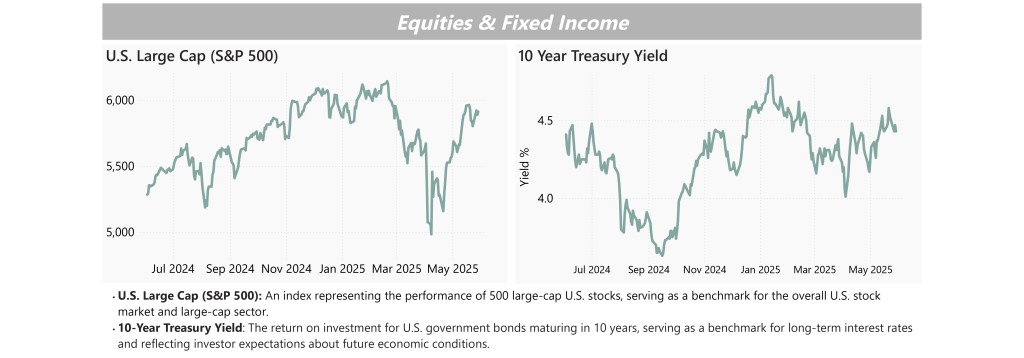

Equity markets rebounded impressively in May. In a sharp reversal of the typical “sell in May” narrative, global stocks rallied as trade tensions abated and recession fears moderated. The MSCI World Index jumped significantly from its 2025 low by mid-month, while the S&P 500 climbed toward a new high for the year (nearing ~5900 by late May). Investors embraced risk assets after the U.S.-China tariff truce removed a major overhang from market sentiment. Cyclical and growth-oriented sectors led the advance, reflecting renewed optimism about the economic outlook and corporate earnings prospects.

By month-end, U.S. equity benchmarks had notched one of their best performances in recent memory, and volatility indices subsided slightly. However, with stocks now pricing in a very optimistic scenario, some caution is warranted. As June begins, the market is entering a historically weak season for equities – a reminder that summer months often bring softer performance after spring rallies. Moreover, underlying risks such as the unresolved trade dispute (once the 90-day ceasefire expires) and central bank policy uncertainty could still trigger turbulence. For now, though, May’s equity melt-up has provided a welcome boost to portfolio values, restoring some confidence that a recession might be averted this year.

Fixed Income

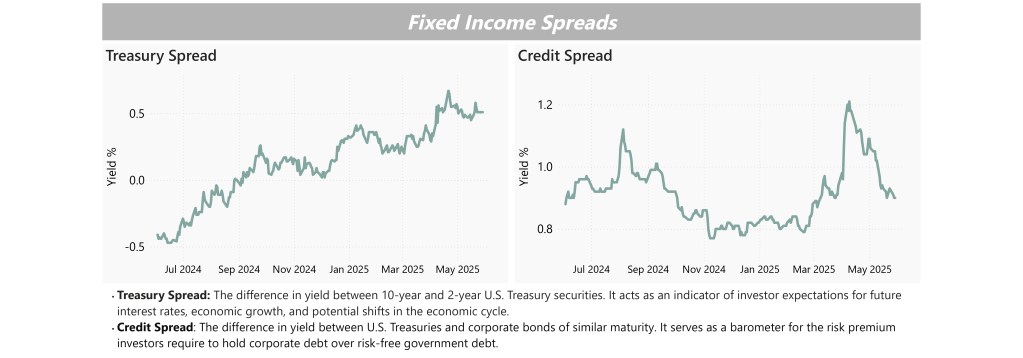

Bond markets saw modest yield increases in May as investors grew more optimistic about the economic outlook. The 10-year U.S. Treasury yield moved higher over the month, while shorter-term yields like the 2-year remained relatively steady¹. Most notably, the 30-year Treasury yield approached 5%—its highest level in nearly two decades—reflecting growing concerns around long-term U.S. debt sustainability and funding requirements.

Credit markets continued their rebound from April’s volatility. Credit spreads tightened meaningfully, with investment-grade spreads falling from a peak near 1.21% in April to around 0.90% by the end of May². Investment-grade bonds returned +1.0% for the month, while high-yield bonds gained +1.1%, driven by a stronger risk backdrop and improving sentiment¹. However, longer-duration bonds have underperformed this year: while the 2-year and 5-year yields have declined meaningfully year-to-date, the 10-year has been more stable, and the 30-year yield has actually risen¹. The combination of tighter spreads and steeper curves signals a more confident outlook in the short and mid-term, but also underscores the pressure building on longer-term debt

Real Estate

The real estate sector continued to feel the strain of high interest rates in May. Housing activity was subdued compared to a year ago, as many buyers remained on the sidelines. In the U.S., existing home sales in April were lower than a year prior, reflecting the affordability challenges posed by elevated borrowing costs. The average 30-year fixed mortgage rate hovered near 7% during May – down from its 7.8% peak in late 2023, but still more than double the ~3% rates of early 2022³. Such stubbornly high financing costs have kept housing demand in check.

There are a few hopeful signs. Housing supply has started to improve – inventories of homes for sale are over 20% higher than a year ago, easing some of the scarcity in the market. Moreover, new home sales showed an uptick: +11% in April vs March (and 3.3% above April 2024) as builders offered incentives and prices moderated². These developments suggest the housing market is gradually adjusting. However, until mortgage rates pull back more meaningfully or incomes rise further, any real estate recovery is likely to remain slow and uneven.

Looking Ahead

May 2025 proved to be a pivotal month for the markets, marked by a resurgence in risk

appetite thanks largely to easing trade tensions. Developments such as the Fed’s continued rate pause and the U.S.-China tariff truce have reinforced hopes that the economy can navigate the coming months without a severe downturn. Indeed, some forecasters now put the odds of a U.S. recession at only around 50/50, and the market’s strong performance suggests investors are leaning toward a cautiously optimistic scenario.

Nonetheless, it is too early to declare victory. The 90-day trade truce will expire later this summer, and the final outcome of negotiations with China, the UK, and other countries remains uncertain. Inflation, though off its peak, is still above target, which could limit central banks’ flexibility if growth falters. As we move into the summer, our team will continue to monitor these evolving risks and opportunities, keeping you informed as conditions change.

1 Allen, Henry and Jim Reid. “April 2025 Performance Review.” Deutsche Bank Research, May 1, 2025.

2 Bloomberg – Points of Return newsletter (May 1-May 31, 2025)

3 Deutsche Bank – Early Morning Reid newsletter (May 1-May 31, 2025)

IMPORTANT DISCLOSURE: This article is produced by Ceva Capital LLC dba Ceva Advisors. The information contained in this report is informational and intended solely to provide educational content to our clients and other readers that we find relevant and interesting. Opinions expressed are just that, and are current only as of the data of publication Nothing in this document should be construed as investment advice; we provide advice on an individualized basis only after understanding your circumstances and needs. The information presented in this newsletter is based on reports from Deutsche Bank and Bloomberg’s ‘5 Things You Need to Know to Start Your Day’ series. Data provided comes from sources we believe are reliable, but accuracy is not guaranteed. Discussion of sectors and the performance of region-specific equities and bonds generally refers to market indices. We use the S&P 500 to represent US large-cap; the Willshire Small Cap to represent US small-cap; the MSCI ACWI ex US to represent international equities; the US 10-year Treasury Yield to represent US Treasuries; the ICE BofA European Government Bond Index to represent European bonds; the ICE BofA US Corporate Index Effective Yield to represent investment-grade bonds; the ICE BofA US High Yield Index Effective Yield to represent high-yield bonds. Indices are unmanaged, are not subject to investment management fees or transaction costs, and it is not possible to invest in an index. Index performance can provide general information about how a particular region or investment has performed, but does not provide information about the performance of Ceva’s client portfolios. Actual client performance may differ materially from the index performance discussed. Past performance is not a guarantee of future results. Financial planning is a tool that can help clients consider different current and future scenarios and construct portfolios designed to meet specific goals and address specific risks. Financial planning does not guarantee a positive outcome or prevent loss. It’s important to revisit financial plans and the underlying assumptions of those plans regularly, and to make adjustments as needed to respond to changing circumstances.