Key Highlights: Navigating July of 2025

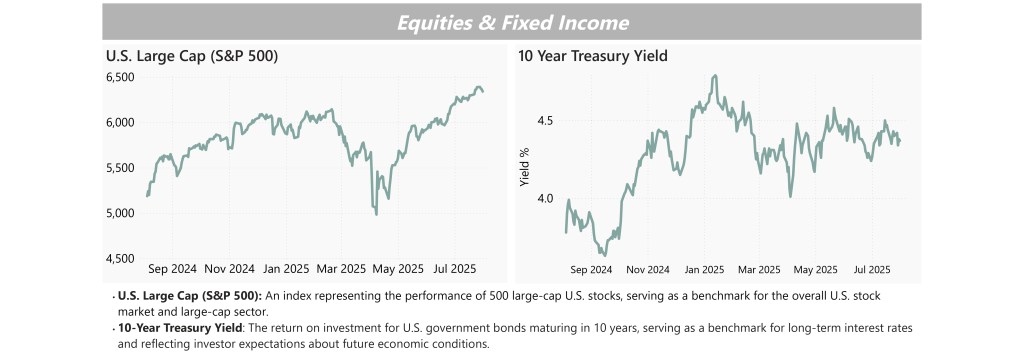

- Equities: The S&P 500 gained 2.2% in July, driven by strong earnings and continued outperformance from large cap tech.

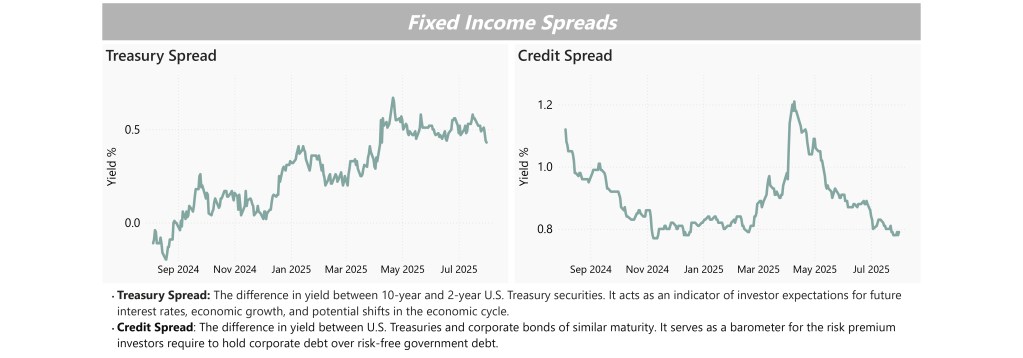

- Fixed Income: Treasury yields moved sideways for the month while credit spreads narrowed for a second month, signaling steady investor appetite for risk.

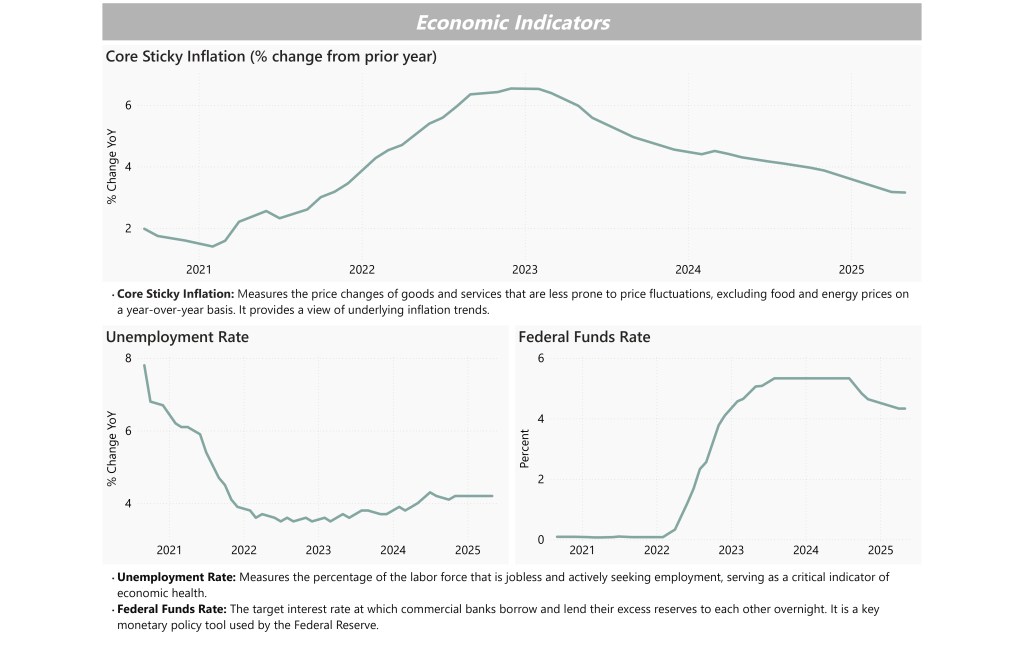

- Economics: Inflation edged higher and the labor market held firm, with rate cut expectations rising sharply after weaker jobs data released at the start of August.

Economics, Equities, and Fixed Income

July offered a relatively calm backdrop after the volatility earlier in the summer. The S&P 500 advanced 2.2%, driven by continued strength in large cap tech and optimism around corporate earnings.1 Market breadth remained narrow, with the “Magnificent 7” continuing to lead index performance and highlighting growing concentration risk within equities.1

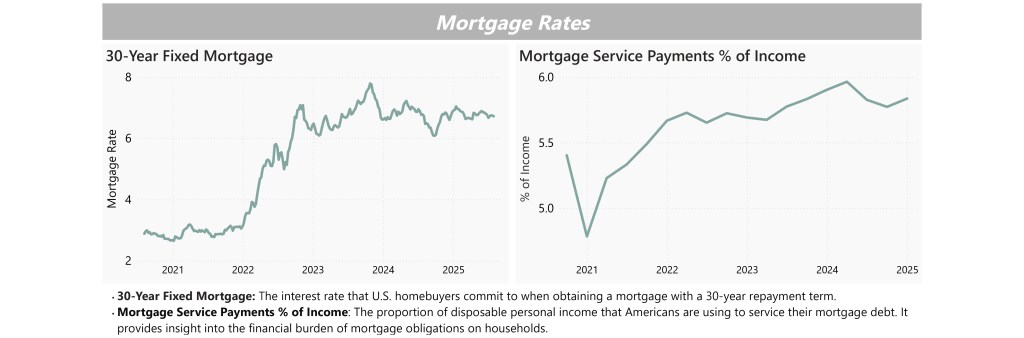

In fixed income, yields were stable as the 10 year Treasury traded between 4.26% and 4.50%. Credit spreads narrowed for a second consecutive month, suggesting continued investor comfort with risk assets. Mortgage rates and servicing costs remained steady, supported by a healthy consumer balance sheet and consistent demand.

The Fed left rates unchanged in July, but inflation remained a concern. Core PCE for June rose to 2.8%, its highest reading in several months, raising questions about how quickly inflation will return to target.2

Interpreting the Current Environment

July demonstrated that markets can deliver steady performance even with unresolved macro risks. Equities advanced, credit markets remained constructive (with positive moves on August 1st), and economic data pointed to continued growth.2 Still, investors should remain aware of several crosscurrents:

- Persistent inflationary pressures

- Policy and trade uncertainty

- Narrow leadership in equity markets

- Long term fiscal and structural concerns

Rick Rieder of BlackRock recently described today’s conditions through a helpful analogy: distinguishing between “potholes” and “sinkholes.”

- Potholes refer to normal short term volatility or market pullbacks based on news flow or data surprises.

- Sinkholes, by contrast, signal deeper structural imbalances or systemic cracks that threaten the foundation of market stability.

So far, we are seeing potholes but no clear sinkholes. The consumer remains solid, the labor market is relatively healthy, and earnings have generally exceeded expectations. Still, after the strong run in equities this year and with seasonal volatility often picking up in late summer, we may encounter a few potholes ahead.

Looking Ahead

While July closed on a stable note, the first day of August introduced fresh volatility. A downward revision to prior months’ job growth released on August 1 caught markets off guard:

- The S&P 500 dropped nearly 2% intraday

- The 10 year Treasury yield fell to 4.22%, its sharpest one day drop in nearly a year

- Expectations for a September rate cut surged, pushing short term bond prices higher

This episode underscores how quickly sentiment can shift based on new data. As we move into the fall, maintaining diversified exposure and a balanced approach to risk will be critical for navigating a potentially choppier environment.

Reach out to someone on our team if you are interested in seeing how you can work to align your portfolio with your goals in the rest of 2025 and beyond.

1 Allen, Henry and Jim Reid. “July 2025 Performance Review.” Deutsche Bank Research, August 1, 2025.

2 “Markets Daily: July 1 – July 31, 2025 Series.” Bloomberg, July 1 – July 31, 2025.

IMPORTANT DISCLOSURE: This article is produced by Ceva Capital LLC dba Ceva Advisors. The information contained in this report is informational and intended solely to provide educational content to our clients and other readers that we find relevant and interesting. Opinions expressed are just that, and are current only as of the data of publication Nothing in this document should be construed as investment advice; we provide advice on an individualized basis only after understanding your circumstances and needs. The information presented in this newsletter is based on reports from Deutsche Bank and Bloomberg’s ‘5 Things You Need to Know to Start Your Day’ series. Data provided comes from sources we believe are reliable, but accuracy is not guaranteed. Discussion of sectors and the performance of region-specific equities and bonds generally refers to market indices. We use the S&P 500 to represent US large-cap; the Willshire Small Cap to represent US small-cap; the MSCI ACWI ex US to represent international equities; the US 10-year Treasury Yield to represent US Treasuries; the ICE BofA European Government Bond Index to represent European bonds; the ICE BofA US Corporate Index Effective Yield to represent investment-grade bonds; the ICE BofA US High Yield Index Effective Yield to represent high-yield bonds. Indices are unmanaged, are not subject to investment management fees or transaction costs, and it is not possible to invest in an index. Index performance can provide general information about how a particular region or investment has performed, but does not provide information about the performance of Ceva’s client portfolios. Actual client performance may differ materially from the index performance discussed. Past performance is not a guarantee of future results. Financial planning is a tool that can help clients consider different current and future scenarios and construct portfolios designed to meet specific goals and address specific risks. Financial planning does not guarantee a positive outcome or prevent loss. It’s important to revisit financial plans and the underlying assumptions of those plans regularly, and to make adjustments as needed to respond to changing circumstances.