Welcome to the September 2024 edition of Ceva Insights. This month was marked by significant market volatility, with a focus on central bank actions and mixed economic data. Despite mid-month fluctuations, global equities showed resilience, supported by strong sector performance and an impactful 50-basis point rate cut by the Federal Reserve.

Key Highlights: Navigating September of 2024

Economic Overview: U.S. GDP for Q2 was revised up to 3.0%, while core CPI remained steady at 0.2%. The Fed cut interest rates by 50 basis points, though broader rate reductions may take time.

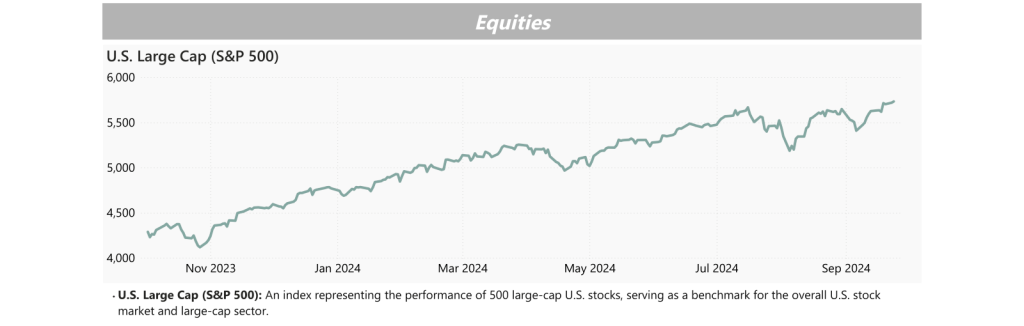

Equities: The S&P 500 gained 2.1%, led by utilities, industrials, and financials. Small caps (Russell 2000) recovered mid-month, closing up 0.7%, with global markets also rallying on stimulus hopes.

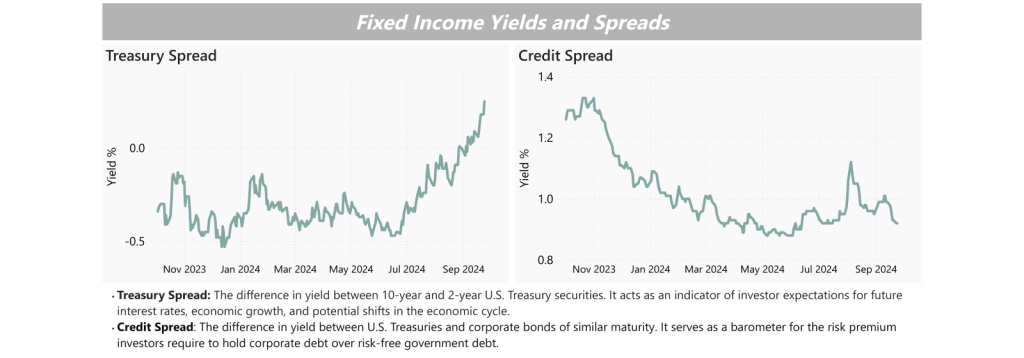

Fixed Income: Treasury yields widened, signaling growth optimism. Credit spreads widened early but tightened by month-end, driven by the Fed’s rate cut.

Real Estate: Industrial and multifamily demand remained strong, while office spaces struggled. The Fed’s rate cut may boost residential real estate, though impacts are yet to be seen.

Economic Overview

September 2024 presented a complex economic environment, marked by significant market shifts driven by mixed economic data and central bank actions. The U.S. GDP for Q2 was revised upward to 3.0%, signaling stronger-than-expected growth, while inflation continued to ease, with core CPI holding steady at 0.2%.

A major development this month was the Federal Reserve’s decision to implement a 50-basis point rate cut, the first since March 2020, aimed at calming recession fears. While the drop in the Fed funds rate is expected to influence borrowing costs across the economy, it’s important to note that other rates, such as mortgage and business loan rates, may not fall as quickly or by the same amount. The Fed’s move provides a signal to the market, but adjustments in other interest rates will depend on factors like lender policies and broader economic conditions.

GDP Growth: Revised up to 3.0% for Q2.

Inflation: Core CPI remained at 0.2%, signaling easing pressures.

Fed Action: A 50-basis point rate cut, though other interest rates may not fall as quickly or by the same amount.

Equities

September 2024 saw global equity markets navigate through volatility, ending the month with moderate gains. The S&P 500 advanced 2.1%, supported by strong performance in sectors such as utilities, industrials, and financials. The tech sector, particularly the “Magnificent 7,” experienced a pullback after months of strong gains, reflecting a shift in market sentiment.

Small-cap stocks, represented by the Russell 2000, experienced a mid-month drawdown but demonstrated resilience, closing the month up 0.7%. Chinese equities rallied, boosted by government stimulus efforts, while European markets posted moderate gains as investors responded to hopes of further economic stimulus measures.

S&P 500: Gained 2.1%, driven by utilities, industrials, and financials.

Small Caps: Russell 2000 rebounded, closing up 0.7% after mid-month losses.

Global Markets: Chinese and European equities rallied, aided by stimulus efforts.

Fixed Income

September 2024 was a strong month for the fixed income market, driven by expectations of further rate cuts and shifting monetary policy. U.S. Treasuries extended their gains for the fifth consecutive month as investors anticipated more accommodative moves from the Federal Reserve.

Treasury spreads widened during the month, reflecting improved growth expectations and a steepening yield curve. Credit spreads initially widened due to economic concerns but later narrowed as market sentiment improved following the Fed’s decision. European sovereign bonds also saw moderate gains, supported by expectations of continued monetary easing.

Treasury Yields: Widened, signaling growth optimism.

Credit Spreads: Widened early but tightened by month-end.

Sovereign Bonds: U.S. Treasuries extended gains, and Euro bonds posted moderate increases.

Real Estate Focus

The real estate market in September 2024 remained stable, with industrial and multifamily properties seeing continued growth, while office spaces struggled due to ongoing hybrid work trends. The Federal Reserve’s rate cut is expected to ease financing costs and potentially boost residential real estate, though the full impact is yet to be seen. Overall, commercial real estate had mixed results, with industrial properties leading.

Industrial and Multifamily: Continued growth from strong fundamentals.

Office Spaces: Struggled due to hybrid work patterns.

Rate Cuts: Expected to support residential real estate.

Closing Remarks

September 2024 highlighted the importance of staying agile in an evolving financial landscape. With central bank actions, economic uncertainty, and market volatility driving much of the month’s movements, investors need to remain proactive and informed. While sectors like equities and fixed income showed resilience, opportunities also exist in alternative investments like real estate.

As we look ahead, maintaining a diversified strategy will be key to navigating potential challenges and taking advantage of emerging opportunities. Thank you for joining us in this month’s review, and we look forward to keeping you informed in the months to come.

Allen, Henry and Jim Reid. “September 2024 Performance Review.” Deutsche Bank Research, October 1, 2024

Goodman, David. “5 Things You Need to Know to Start Your Day: September 1 – September 30, 2024 Series.” Bloomberg, September 1 – September 30, 2024.

IMPORTANT DISCLOSURE: The information contained in this report is informational and intended solely to provide educational content to our clients and other readers that we find relevant and interesting. Opinions expressed are just that, and are current only as of the data of publication Nothing in this document should be construed as investment advice; we provide advice on an individualized basis only after understanding your circumstances and needs. The information presented in this newsletter is based on reports from Deutsche Bank and Bloomberg’s ‘5 Things You Need to Know to Start Your Day’ series. Data provided comes from sources we believe are reliable, but accuracy is not guaranteed. Discussion of sectors and the performance of region-specific equities and bonds generally refers to market indices. We use the S&P 500 to represent US large-cap; the Willshire Small Cap to represent US small-cap; the MSCI ACWI ex US to represent international equities; the US 10-year Treasury Yield to represent US Treasuries; the ICE BofA European Government Bond Index to represent European bonds; the ICE BofA US Corporate Index Effective Yield to represent investment-grade bonds; the ICE BofA US High Yield Index Effective Yield to represent high-yield bonds. Indices are unmanaged, are not subject to investment management fees or transaction costs, and it is not possible to invest in an index. Index performance can provide general information about how a particular region or investment has performed, but does not provide information about the performance of Ceva’s client portfolios. Actual client performance may differ materially from the index performance discussed. Past performance is not a guarantee of future results. Financial planning is a tool that can help clients consider different current and future scenarios and construct portfolios designed to meet specific goals and address specific risks. Financial planning does not guarantee a positive outcome or prevent loss. It’s important to revisit financial plans and the underlying assumptions of those plans regularly, and to make adjustments as needed to respond to changing circumstances.