November Recap and December Outlook

The shutdown is over, but it’s taking time to get the data flowing again. September data will likely be available in early December, and October will be combined with November on a mid-December release. The Federal Reserve wrapped up the year with an early December meeting, at which they delivered a quarter-point interest rate cut, following consensus expectations.

With the absence of official data, private sector data from ADP and other sources is attempting to fill the gap.

It’s been an eventful year, and the ongoing difficult economic backdrop that includes tariffs, slow progress on normalizing interest rates and a very cautious consumer is beginning to create a bifurcation between how large and small businesses are holding up.

Let’s get into the data – what there is of it:

- The shutdown again meant no government labor statistics. The Chicago Fed’s estimate of the unemployment rate, which combines public-sector with private-sector data, fell slightly from the October estimate, to 4.44% from 4.46%.

- Looking only at private-sector employment, ADP reported a loss of 32,000 jobs in November. This reverses the gains in October and returns to the trend of contracting labor market data.

- The University of Michigan Consumer Sentiment Index rose by 2 percentage points. Upward movement is a good sign, but it is still off a very low reading. Labor market expectations remained “dismal.”

- The Atlanta Fed’s GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 3.5 percent.

What Does the Data Add Up To?

The Fed’s final meeting of the year brought a 25 basis point rate cut, which investors had pretty much priced into the markets.

A conservative cut seemed prudent, given that the famously data-driven Fed under Chairman Powell had to make the decision without access to much of the traditional government data. This marked the third cut in 2025, following 25 basis point cuts in September and October.

Attention now turns to 2026, and the path of rates is not exactly clear. Payroll processor ADP reported the loss of 32,000 jobs in November, and all of those losses were from firms with fewer than 50 employees. The pressure isn’t just on cutting labor. A recent Bloomberg report found that bankruptcy filings for small businesses, under a federal program called Subchapter V that allows companies to shed debt more quickly, are at a higher level than at any point in the program’s six-year history.

Large companies have more resources and so far have been able to backstop the labor market. Small companies are much more vulnerable, and the impact of shedding jobs and closing their doors may be more difficult to undo, even if the Fed determines it is necessary to cut rates more quickly in 2026.

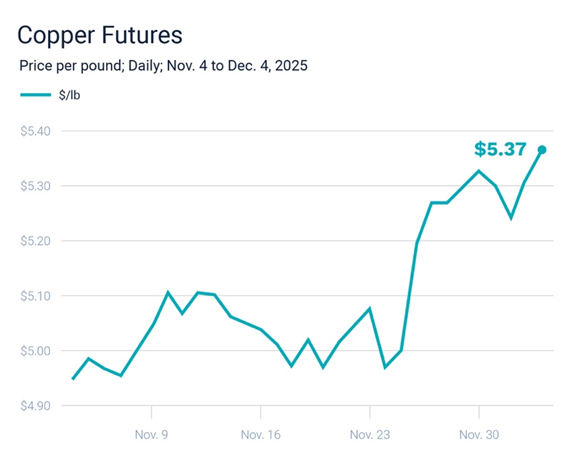

Chart of the Month: Copper Prices Rally

Copper is sometimes called “Doctor Copper,” as the metal is used so broadly that it can be seen as a barometer of the health of the economy. Increased demand is usually interpreted as a sign that the economy is growing. This time, however, it is unclear if the demand is organic, or driven by worries over tariffs and supply chain disruptions.

Source: Axios

Equity Markets in November

- The S&P 500 was up 0.13%% for the month

- The Dow Jones Industrial Average gained 0.32% for the month

- The S&P MidCap 400 rose 1.92% for the month

- The S&P SmallCap 600 gained 2.51% for the month

Source: S&P Global. All performance as of November 30, 2025.

Eight of the eleven S&P 500 sectors had positive returns. Breadth was positive, with 324 issues gaining, up from 204 in October. Health Care was the strongest performer, up 9.14% for the month. Information Technology fell victim to profit-taking, ending the month down 4.36%, the second worst month of the year, behind March, for the sector. YTD, all eleven sectors are up as we go into the last month of the year. Communication services is the year-to-date leader, up 33.83%, and Real Estate is bringing up the rear at 2.51%

Bond Markets in October

The 10-year U.S. Treasury ended the month at a yield of 4.02%, down from 4.09% the prior month. The 30-year U.S. Treasury ended November at 4.67%, up from 4.66%. The Bloomberg U.S. Aggregate Bond Index returned 0.62%. The Bloomberg Municipal Bond Index returned 0.32%.

The Smart Investor

As you get to the end of the year, it’s a good time to think about your financial plan. What worked and what didn’t? What changes do you need to make? Think through:

- Did any major life events occur (or begin to take shape) that should prompt updates to your plan?

- Has your comfort with investment risk changed after experiencing this year’s markets?

- Is your current portfolio still aligned with your long-term objectives?

- How did your financial decisions this year move you closer to or further from your long-term goals?

- What new goals or priorities should be incorporated for next year?

Have any big expectations changed? For example, retirement dates, having one spouse reduce work, children needing more expensive education?

Your financial plan should include your goals, expectations and assumptions, a clear idea of the level of risk you are comfortable with, and both a strategic and a tactical asset allocation. As your situation and expectations change, your plan will need to be updated to keep you on track.

If you want to see how these questions impact your financial situation, our team at Ceva Advisors would love to help. You can reach out to our team through our website to start a conversation today and learn how we can apply these insights to your unique situation.

IMPORTANT DISCLOSURE: This article is produced by Ceva Capital LLC dba Ceva Advisors. The information contained in this report is informational and intended solely to provide educational content to our clients and other readers that we find relevant and interesting. Opinions expressed are just that, and are current only as of the data of publication Nothing in this document should be construed as investment advice; we provide advice on an individualized basis only after understanding your circumstances and needs. Data provided comes from sources we believe are reliable, but accuracy is not guaranteed. Discussion of sectors and the performance of region-specific equities and bonds generally refer to market indices. We use the S&P 500 to represent US large-cap; the Willshire Small Cap to represent US small-cap; the MSCI ACWI ex US to represent international equities; the US 10-year Treasury Yield to represent US Treasuries; the ICE BofA European Government Bond Index to represent European bonds; the ICE BofA US Corporate Index Effective Yield to represent investment-grade bonds; the ICE BofA US High Yield Index Effective Yield to represent high-yield bonds. Indices are unmanaged, are not subject to investment management fees or transaction costs, and it is not possible to invest in an index. Index performance can provide general information about how a particular region or investment has performed, but does not provide information about the performance of Ceva’s client portfolios. Actual client performance may differ materially from the index performance discussed. Past performance is not a guarantee of future results. Financial planning is a tool that can help clients consider different current and future scenarios and construct portfolios designed to meet specific goals and address specific risks. Financial planning does not guarantee a positive outcome or prevent loss. It’s important to revisit financial plans and the underlying assumptions of those plans regularly, and to make adjustments as needed to respond to changing circumstances.