Key Highlights: Navigating August of 2025

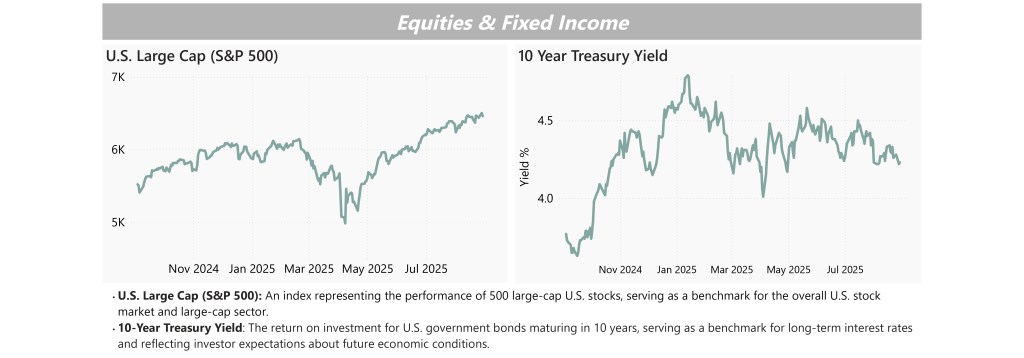

- Stocks: The market continued its climb in August, with the S&P 500 finishing the month up about 2%.

- Bonds: Interest rates moved lower, especially on shorter-term bonds, reflecting expectations that the Federal Reserve may cut rates.

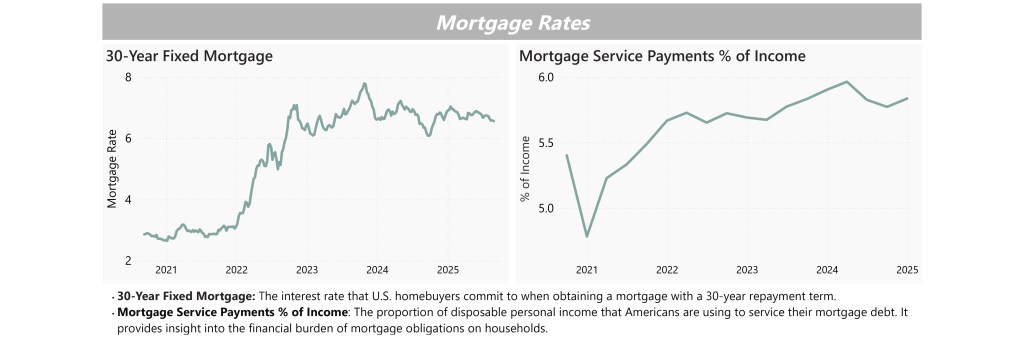

- Credit and Housing: Corporate borrowing costs remained steady, showing investors remain confident in company balance sheets. Mortgage rates also ticked down a little, easing pressure on homebuyers.

Markets Recap: What Happened and Why

Equities spent August grinding higher. The S&P 500 began the month at its low on August 1 and advanced steadily into August 28, the monthly high, supported by a calmer inflation backdrop and growing expectations that the Federal Reserve could move toward easier policy. A modest pullback on August 29 still left the month higher overall. Under the surface there were as many up days as down days, which signals a healthy two way market that rewarded patience rather than a one day surge.

In fixed income markets, the front end did most of the moving. The 2 year yield rose into August 21 and then fell sharply into month end, with its largest daily drop of 12 basis points on August 26. The 10 year yield moved in a much narrower corridor, peaking near August 18 and easing into the finish. Because short rates fell more than long rates, the yield curve between the 10 year and 2 year steepened through the second half of the month. Credit spreads told a constructive story overall. Investment grade OAS narrowed through mid month to 0.75 percent before giving back a couple of basis points into month end. Mortgage rates stepped lower on each weekly print in August.1

Interpreting the Current Environment

When looking at the current environment, there are three main themes investors should keep in mind.

- Momentum with guardrails. Equities climbed through most of August but did so with balanced up and down days. That pattern is consistent with an advance that is being checked by ongoing macro questions rather than a rush of speculative buying.

- Policy expectations are doing the heavy lifting at the front end. The sharper decline in the 2 year versus the 10 year says the market is leaning toward easier policy ahead.1 The curve steepened because short rates fell more than long rates, not because long rates spiked. That is a friendlier version of steepening for risk assets.

- Credit conditions remain constructive. A mid-month tight in OAS with only a small giveback into month end suggests companies still enjoy supportive financing conditions, even as investors remain selective.

The environment still presents risks that can cause short-term swings, but overall conditions remain supportive enough for markets to move forward.

Looking Ahead

As September begins, investors will focus on whether the Fed formalizes an easier policy stance and on whether incoming inflation and labor data confirm the late August move in the front end.2 Watch for any shift in earnings guidance as companies look toward year end, and for whether credit spreads stay anchored near recent tights.

1 Allen, Henry and Jim Reid. “August 2025 Performance Review.” Deutsche Bank Research, September 1, 2025.

2 “Markets Daily: August 1 – August 31, 2025 Series.” Bloomberg, August 1 – August 31, 2025.

IMPORTANT DISCLOSURE: This article is produced by Ceva Capital LLC dba Ceva Advisors. The information contained in this report is informational and intended solely to provide educational content to our clients and other readers that we find relevant and interesting. Opinions expressed are just that, and are current only as of the data of publication Nothing in this document should be construed as investment advice; we provide advice on an individualized basis only after understanding your circumstances and needs. The information presented in this newsletter is based on reports from Deutsche Bank and Bloomberg’s ‘5 Things You Need to Know to Start Your Day’ series. Data provided comes from sources we believe are reliable, but accuracy is not guaranteed. Discussion of sectors and the performance of region-specific equities and bonds generally refers to market indices. We use the S&P 500 to represent US large-cap; the Willshire Small Cap to represent US small-cap; the MSCI ACWI ex US to represent international equities; the US 10-year Treasury Yield to represent US Treasuries; the ICE BofA European Government Bond Index to represent European bonds; the ICE BofA US Corporate Index Effective Yield to represent investment-grade bonds; the ICE BofA US High Yield Index Effective Yield to represent high-yield bonds. Indices are unmanaged, are not subject to investment management fees or transaction costs, and it is not possible to invest in an index. Index performance can provide general information about how a particular region or investment has performed, but does not provide information about the performance of Ceva’s client portfolios. Actual client performance may differ materially from the index performance discussed. Past performance is not a guarantee of future results. Financial planning is a tool that can help clients consider different current and future scenarios and construct portfolios designed to meet specific goals and address specific risks. Financial planning does not guarantee a positive outcome or prevent loss. It’s important to revisit financial plans and the underlying assumptions of those plans regularly, and to make adjustments as needed to respond to changing circumstances.