Welcome to the August 2024 edition of Ceva Insights – your comprehensive overview of the latest market trends and financial developments. August was marked by significant volatility, with events such as a weak US jobs report and a dramatic slump in Japanese markets contributing to early uncertainty. However, a dovish tone from Fed Chair Powell at the Jackson Hole symposium helped restore investor confidence, leading to gains in equities and bonds by month’s end. In this edition, we explore key economic insights, market movements, and investment opportunities to help you navigate these dynamic conditions.

Key Highlights: Navigating August of 2024

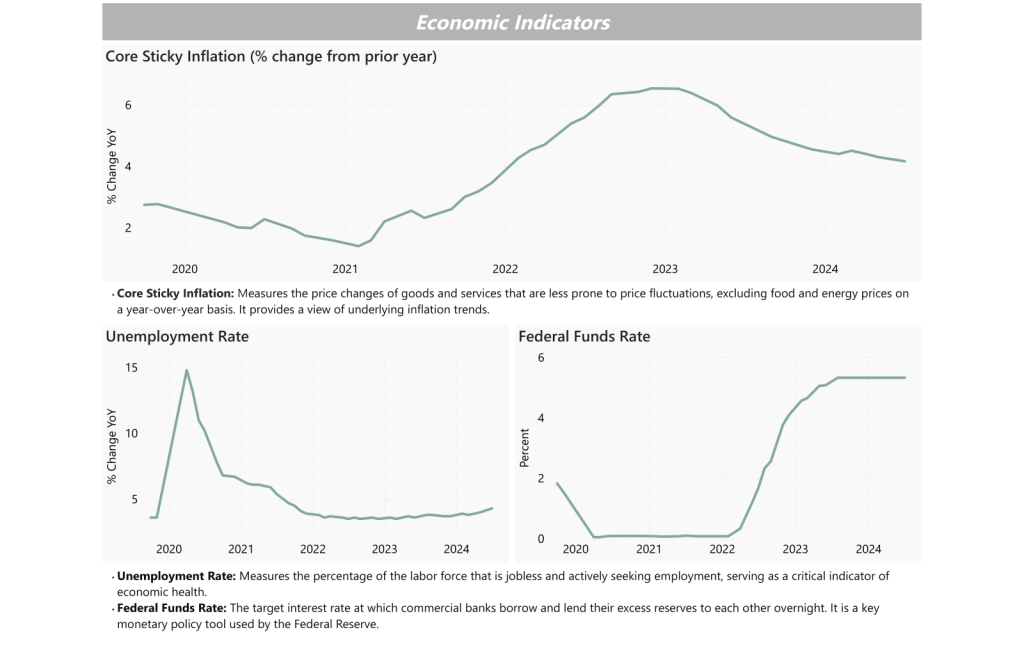

Economic Overview: August saw significant market volatility, with the VIX spiking to levels not seen since March 2020 due to recession fears. GDP growth for Q2 was revised up to 3.0%, while core CPI remained low at 0.2%, signaling easing inflation pressures.

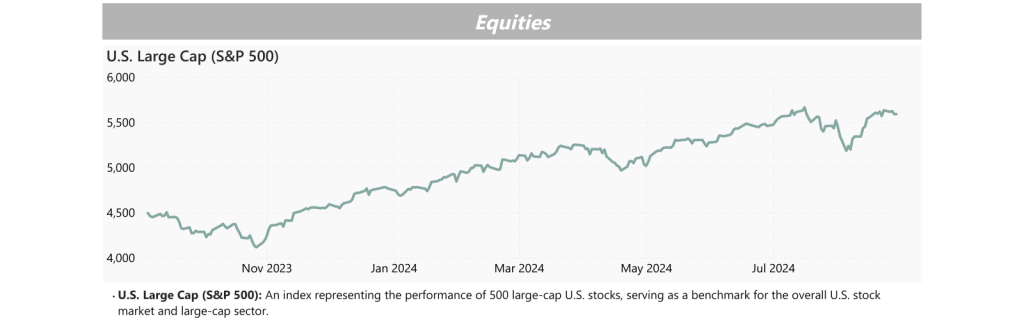

Equities: The S&P 500 gained 2.4%, bringing year-to-date gains to 19.5%, while the Russell 2000 recovered most early losses to close down 1.6%, highlighting the market’s resilience amid uncertainty.

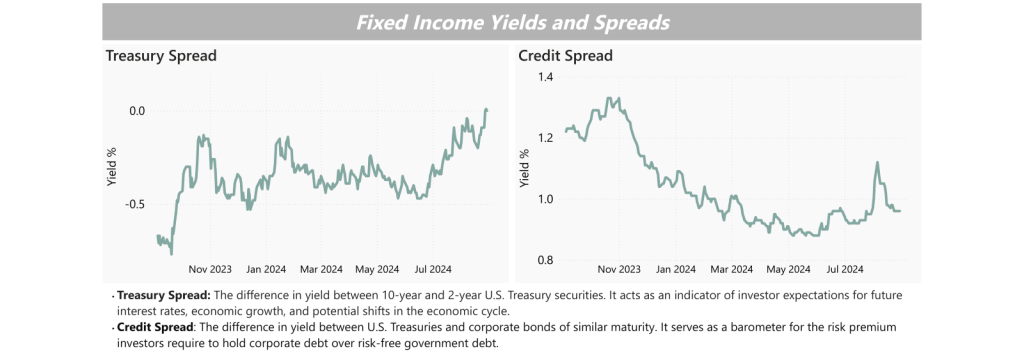

Fixed Income: U.S. Treasuries gained 1.3% as Treasury spreads tightened and credit spreads narrowed, reflecting expectations of slower growth and potential Fed rate cuts.

Commodities: Gold surged above $2,500 per ounce amid rate cut expectations, while oil prices remained volatile due to geopolitical tensions and fluctuating demand.

Economic Overview

August 2024 saw significant market volatility, driven by a weak US jobs report that sparked fears of a potential recession. The VIX (volatility index) index spiked to levels last seen in March 2020, and the unwinding of the yen carry trade led to sharp declines in Japanese markets. However, the situation stabilized later in the month with better-than-expected economic data and a dovish message from Fed Chair Jerome Powell at the Jackson Hole symposium.

The U.S. GDP growth rate for Q2 was revised up from 2.8% to 3.0%, indicating stronger economic momentum, while core CPI remained low at 0.2%, suggesting easing inflationary pressures. Despite calls for an emergency rate cut, the Fed held rates steady. However, Powell’s comments have increased expectations for a rate cut in September.

GDP Growth: Revised up to 3.0% for Q2.

Inflation: Core CPI at 0.2%, signaling easing pressures.

Market Volatility: VIX had an incredible spike but stabilized after Powell’s remarks.

Equities

In August 2024, equity markets displayed significant volatility but ultimately posted gains. The S&P 500 continued its upward trend, gaining 2.4% for the month, bringing its year-to-date return to 19.5%. This marks the fourth consecutive month of gains for the index, underscoring its resilience amid uncertainty. The Russell 2000 had a challenging start, dropping as much as 9.5% in the first few days due to heightened market fears. However, the small-cap index managed to recover most of its losses, closing the month down just 1.6%.

Global markets also reflected the mixed sentiment, with Europe’s STOXX 600 up 1.6%, while Japan’s Nikkei fell by 1.1%, largely due to the early-month turmoil. The swings in equities highlighted the market’s sensitivity to economic data and central bank signals, particularly around the potential for rate cuts by the Fed.

S&P 500: Gained 2.4% in August, up 19.5% YTD.

Small Caps: Russell 2000 fell 9.5% early in the month, closing down 1.6%.

Global Markets: STOXX 600 up 1.6%; Nikkei down 1.1%.

Fixed Income

August 2024 saw notable shifts in the fixed income market, driven by changing expectations for monetary policy and market volatility. U.S. Treasuries gained 1.3% for the month as investors anticipated potential Fed rate cuts. Treasury spreads tightened significantly, signaling expectations of slower growth and potential rate cuts, while credit spreads initially widened sharply due to inflation concerns but later tightened as market sentiment improved.

Treasury Spreads: Tightened throughout the month, reflecting expectations of slower growth.

Credit Spreads: Initially widened, then narrowed as market conditions stabilized.

Sovereign Bonds: U.S. Treasuries up 1.3%, Euro sovereigns up 0.4%.

Closing Remarks

August brought unexpected turns and heightened market volatility, underscoring the unpredictable nature of the financial landscape. From sharp equity swings to shifting bond yields, the month has been a reminder of the need to stay alert and adaptable. With all eyes on the potential Fed actions in September, the coming months promise to be just as dynamic.

As always, staying informed is key. Thank you for joining us in navigating August’s developments, and we look forward to providing further insights in our next edition.

Allen, Henry and Jim Reid. “August 2024 Performance Review.” Deutsche Bank Research, September 2, 2024

Goodman, David. “5 Things You Need to Know to Start Your Day: August 1 – August 31, 2024 Series.” Bloomberg, August 1 – August 31, 2024.

IMPORTANT DISCLOSURE: The information contained in this report is informational and intended solely to provide educational content to our clients and other readers that we find relevant and interesting. Opinions expressed are just that, and are current only as of the data of publication Nothing in this document should be construed as investment advice; we provide advice on an individualized basis only after understanding your circumstances and needs. The information presented in this newsletter is based on reports from Deutsche Bank and Bloomberg’s ‘5 Things You Need to Know to Start Your Day’ series. Data provided comes from sources we believe are reliable, but accuracy is not guaranteed. Discussion of sectors and the performance of region-specific equities and bonds generally refers to market indices. We use the S&P 500 to represent US large-cap; the Willshire Small Cap to represent US small-cap; the MSCI ACWI ex US to represent international equities; the US 10-year Treasury Yield to represent US Treasuries; the ICE BofA European Government Bond Index to represent European bonds; the ICE BofA US Corporate Index Effective Yield to represent investment-grade bonds; the ICE BofA US High Yield Index Effective Yield to represent high-yield bonds. Indices are unmanaged, are not subject to investment management fees or transaction costs, and it is not possible to invest in an index. Index performance can provide general information about how a particular region or investment has performed, but does not provide information about the performance of Ceva’s client portfolios. Actual client performance may differ materially from the index performance discussed. Past performance is not a guarantee of future results. Financial planning is a tool that can help clients consider different current and future scenarios and construct portfolios designed to meet specific goals and address specific risks. Financial planning does not guarantee a positive outcome or prevent loss. It’s important to revisit financial plans and the underlying assumptions of those plans regularly, and to make adjustments as needed to respond to changing circumstances.